An energy-security trade, not a moral one.

Measured by the revenue that companies earn from environmental products and services, the green economy crossed ten trillion dollars in market value this year. Treated as a single grouping it would rank third in the world, behind only technology and industrials. The obvious interpretation is that this reflects a moral victory. It reads better as a security trade. '

This year’s US-Iran fuel disruptions made the point. The oil price spiked and faded; the dependency it exposed did not. Oil must move, across borders and through choke points someone else controls. An electron does not: made from gas, coal, solar, wind or uranium, once on the grid it carries no record of where it came from. Electrify, and a single point of failure becomes a menu. China priced that early and now barely feels an oil shock; Europe still scarred by 2022 and again this year, has reached the same conclusion. Even the body that built the defining green taxonomy now frames the transition as an energy security as much as decarbonisation. The capital followed the security case, not the reverse.

The flaw inside the rally

The returns are durable, not a fad. Green equities beat the market by 12.4 % in the year ending April 2026 and have outpaced global equities by roughly 133% since 2008, with the large institutional owners moving sustainably from the margins to the centre of asset allocation. But the larger and more standardised the green finance world becomes, the more its definitions become gamed, and the most interesting arbitrage now sits within digital infrastructure.

The reason is a measurement flaw. Every green taxonomy in use scores environmental benefit at the level of the asset and its revenue. It is attributional: it essentially certifies that an entity procures something green. It never actually asks the consequential question, whether the entity leaves the wider system cleaner and less congested, or whether it simply relocates the issue. Carbon accounting already learned this. Work from Princeton and Tsinghua show annual certificate matching does almost nothing for system emissions, because the buyer can claim renewables that would have been built anyway; only hourly matching reliably helps. Capital markets have not made that move, and they face a constraint emissions accounting ignores grid capacity. Connection, not certificates, is the binding limit now, and nobody scores it.

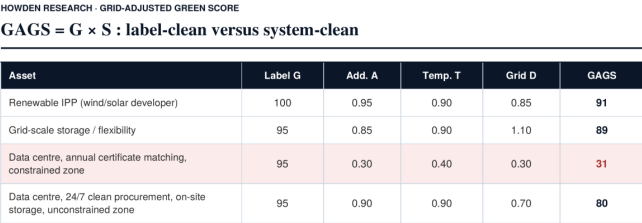

The Grid-Adjusted Green Score

This is Howden Research’s proposed solution, and the original contribution of this analysis. The Grid-Adjusted Green Score (GAGS) discounts an existing green label by a factor of its effect on the system:

Worked example: Consider two data centres that both receive a conventional green score of 90/100 because each procures 100% renewable electricity. Under existing taxonomies, they appear equally “green”. Under GAGS, however, the distinction emerges. Data Centre A signs long-term contracts that finance new renewable capacity, matches its electricity consumption hourly, and operates in a region with spare grid capacity. Its system multiplier (S) is 0.89, giving it a GAGS of 80. Data Centre B relies on annual renewable certificates, adds no new generation, and operates in a highly constrained grid zone where its connection crowds out other demand. Its multiplier falls to 0.34, producing a GAGS of just 31. The environmental label is identical; the system impact is not.

G is the headline green share a taxonomy already produces. S combines three sub-scores: additionality (does procurement add new capacity, or just reallocate existing generation?), temporal matching (hourly or netted annually so the load draws fossil power when renewables are scarce?), and grid contribution (does the asset relieve local network scarcity or book a connection ahead of everyone else?). A starting calibration weights them 0.3, 0.3 and 0.3, with the grid term allowed above one where an asset is a net reliever of constraint.

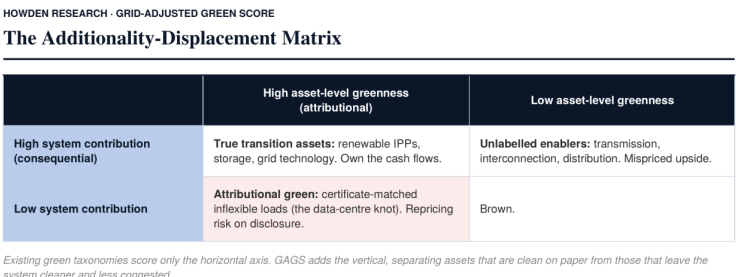

Read the two data centres together: near-identical labels, a fifty-point gap in consequence. The score does not punish data centres; it rewards the ones doing the harder, more costly thing, and prices the gap that a single label hides. The same logic maps onto a metric useful for portfolio construction.

The misplacing takes place in the corners. The market overpays high-attributional names regardless of their system effect, and underpays the enablers, the transmission and storage that receive the constraint everyone is fighting over. GAGS needs hourly metering and connectionzone data that are not yet uniformly disclosed, so it is a direction of travel rather than a finished index, but what it does is that it puts a number on a gap that the market is currently treating as invisible.

The data-centre knot: Slough to East London

Slough compresses the argument into one town: the largest data-centre cluster in Europe, about a gigawatt of compute, roughly 95% backed by renewable contracts. Clean on paper. Yet thirty miles east of the collision is on the record. The London Assembly’s Gridlocked report documents how parts of the West London grid hit full capacity from 2022, with some completed homes in Hillingdon, Hounslow and Ealing were told that they could wait until 2037 for a connection. Data centres are still under a tenth of UK electricity, but a single typical facility draws the power of around a hundred thousand households, and demand is forecast to rise by up to 600% by 2050.

On a GAGS basis, an annual-matched load in a constrained zone scores far below its label, exactly the case the taxonomy was never built to adjudicate. East London is next, with hyperscale capacity pushing into the Docklands. Slough had fourteen years and a council that planned; East London is getting a compressed version of the same choice, with less room to get it wrong.

For investors and insurers

For investors, the names most exposed to a disclosure shock are the high-attributional, lowconsequential ones: certificate-matched inflexible loads, and utilities whose valuations now lean on AI data-centre load growth. The misplaced upside lies with the enablers, the contracted renewable owners valued as bond proxies and the grid and storage names the taxonomy underweighs. An asset class up sharply in eighteen months is not undiscovered; what remains is separating durable cash flow from beta, and the matrix is a map of where that risk hides.

For insurers, three things follow. A development built but unable to energise is a businessinterruption loss contingent on a third party’s grid programme, which makes connection delay a priceable exposure. An insurer writing a green data centre on an attributional basis essentially inserts the bond market’s flaw in its own insured-emissions accounting. And clustering a gigawatt of compute concentrates correlated heat, water and flood exposures into the kind of profile catastrophe modelling exists to price. Each sits closer to where a broker works than the green label suggests.

What happens next

Three forecasts, held at different strengths. The security case is now bipartisan in a way the climate case never was, which makes it durable. The clean-energy and AI fight for grid capacity becomes a fault line inside green portfolios, not only between green finance and its critics, since a fund holding both a solar developer and a data-centre REIT is long both sides of the same dispute. And the one to bet on least and to watch the most, expect the first serious piece of regulation within roughly eighteen months which could force operators to disclose griddisplacement impact alongside their procurement claims. The Hillingdon delay is the kind of human story that turns a connection-queue argument into a political one. The Grid-Adjusted Green Score (GAGS) is a way to be early to that disclosure rather than getting caught out by it.